New Jersey Law Journal: Brace Yourself: RMDs Are Coming

Almost four years after the SECURE Act went into effect, plan administrators, tax practitioners, and certain inherited IRA beneficiaries finally have an answer to the hotly debated question on required minimum distributions (RMDs) for inherited IRAs.

Pursuant to Notice 2024-35, the Internal Revenue Service (the service) approved final Treasury Relation (regulation) Section 1.401(a)(9) on July 18, 2024, answering that question in the affirmative for most IRAs inherited after Jan. 1, 2020. When the SECURE Act went into effect on Jan. 1, 2020, the biggest change to the rules for inherited IRAs was the elimination of stretch out treatment for many IRA beneficiaries. Prior to the SECURE Act, a beneficiary of an inherited IRA was able to “stretch” RMDs over the beneficiary’s lifetime, deferring tax recognition.

The SECURE Act instead gave us the 10-year rule, requiring most inherited IRAs to be fully distributed within 10 years of the death of the plan participant (i.e., the person contributing to the IRA). See I.R.C. Section 401(a)(9)(H)(i). However, until the service issued the final regulation, there was uncertainty as to whether beneficiaries subject to the 10-year would have RMDs or could instead choose when to take distributions from the inherited IRA within 10 years of the plan participant’s death. That open question has been answered by the final regulation.

Understanding that the SECURE Act created considerable confusion, the service waived penalties for failure to take RMDs for inherited IRAs subject to the SECURE Act for the 2020 through 2024 tax years. See I.R.S. Notice 2024-35, 2024, I.R.B. 2024-19. That waiver, however, only applied to IRA beneficiaries that did not have the option to stretch out their inherited IRAs—those beneficiaries subject to the 10-year rule. Starting in 2024, many inherited IRA beneficiaries will have to take RMDs.

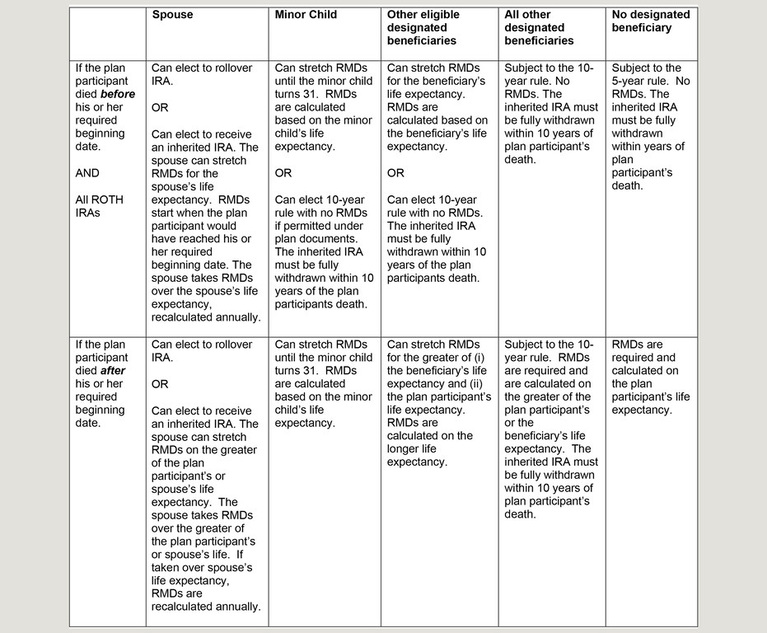

There are three questions to determine whether RMDs are required from an inherited IRA:

Did the plan participant die before or after his or her required beginning date?

The required beginning date is the date a plan participant would be required to start taking RMDs. Generally, the required beginning date is April 1st of the year after the plan participant reaches age 73. However, for a 401k where the plan participant owns less than 5% of the company sponsoring the 401k, the required beginning date is the later of April 1 in the year after the plan participant reached the age of 73 or the plan participant retires.

Is the IRA a traditional IRA (pre-tax funded) or a ROTH IRA (post-tax funded)?

For a ROTH IRA, which is funded by the plan participant with post-tax dollars, the plan participant is not required to take any RMDs during the plan participant’s lifetime.

Because the plan participant is not required to take RMDs from his or her ROTH IRA, the plan participant is deemed to have died before his or her required beginning date in determining RMDs for the beneficiaries of an inherited ROTH IRA.

What is the relationship of the IRA beneficiary to the plan participant?

The SECURE Act created a new beneficiary classification—the eligible designated beneficiary. An eligible designated beneficiary in relation to the plan participant includes a surviving spouse, minor child, chronically ill or disabled person, and a beneficiary who is not more than 10 years younger than the plan participant. See I.R.C. Section 401(a)(9)(E)(ii).

These individuals can stretch out their inherited IRAs, similar to pre-SECURE Act rules. See I.R.C. Section 401(a)(9)(B)(iv). Of all the eligible designated beneficiaries, a surviving spouse and a minor child receive special treatment. A surviving spouse has more advantageous rules to defer RMDs from his or her inherited IRA. See I.R.C. Section 401(a)(9)(H)(ii). Alternatively, a minor child has less advantageous rules. A minor child can only stretch out his or her inherited IRA until 10 years after the minor child obtains the age of majority (i.e., 21). In other words, a minor child beneficiary of an inherited IRA must fully withdraw such IRA by the time he or she obtains the age of 31. See I.R.C. Section 401(a)(9)(E)(iii).

Other designated beneficiaries with respect to the plan participant, such as an adult child, a person more than 10 years younger than the plan participant and all other named beneficiaries of the IRA (excluding charity and the plan participant’s estate), are subject to the 10-year rule. See I.R.C. Section 401(a)(9)(H)(i). Under the 10-year rule, the inherited IRA must be fully withdrawn within 10 years of the plan participant’s death. RMDs for an inherited IRA subject to the 10-year rule are determined if the plan participant died before or after his or her required beginning date.

Finally, an IRA that names an estate, charity, or disqualified trust is deemed to have no designated beneficiary, and is subject to the five-year rule. The final Regulation confirms the SECURE Act did not change the prior five-year rule, and when a plan participant dies before his or her required beginning date, these non-designated beneficiaries must fully withdraw an inherited IRA within five years of the plan participant’s death.

Once those three questions are answered, you can determine the RMDs from an inherited IRA from the table below:

Table showing RMDs from an inherited IRA. Courtesy image.

The rules governing RMDs for inherited IRAs are more nuanced than the table above (the leading authority for IRAs, Natalie Choate, has written a 127-page supplement on RMDs post-SECURE Act). It is essential to speak with a tax practitioner to determine the RMDs for an inherited IRA subject to the SECURE Act rules.

Reprinted with permission from the March 31, 2025 issue of the New Jersey Law Journal. © 2025. ALM Media Properties, LLC. Further duplication without permission is prohibited. All rights reserved.